Key information

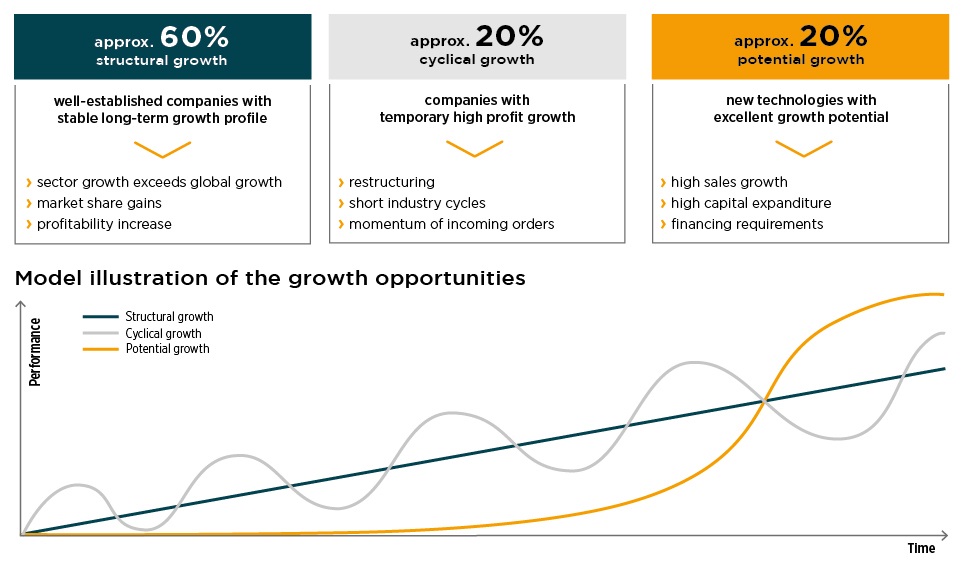

The investment focus of DJE - Mittelstand & Innovation is on high-growth, small- and mid-cap equities from Germany, Austria, and Switzerland. The diversification between structural, cyclical, and potential growth opportunities aims to deliver attractive risk-adjusted returns by investing in innovative niche players and “hidden champions”. The fund invests in a diversified portfolio of 50-80 equities identified through a disciplined fundamental analysis of the companies. DJE - Mittelstand & Innovation is an innovative investment solution for investors that are looking for a growth fund with an attractive risk-reward profile.

Responsible manager since 01/10/2022

Key information

| ISIN: | LU1227570485 |

| WKN: | A14SK1 |

| Category: | Fund Europe Small-Cap Equity |

| Minimum Equity: | 51% |

| Partial Exemption of Income ¹: | 30% |

| VG/KVG: | DJE Investment S.A. |

| Fund Management: | DJE Kapital AG |

| Risk Category: | 4 |

| This sub-fund/fund promotes ESG features in accordance with Article 8 of the Disclosure Regulation (EU Nr. 2019/2088). | |

| Type of Share: | accumulation |

| Financial Year: | 01.01. - 31.12. |

| Launch Date: | 03/08/2015 |

| Fund currency: | EUR |

| Fund Size (16/05/2024): | 84,42 Mio EUR |

| TER p.a. (29/12/2023): | 1,90 % |

| Reference Index: | - |

Fees

| Management Fee p.a.: | 1,450 % |

| Custodian Fee p.a.: | 0,060 % |

Ratings & Awards (16/05/2024)

| Morningstar*: |

|

|

Awards: €uro Eco Rating A Finanzen Verlag, Mountain View Q2 2023 |

All ESG information presented here relates to the fund portfolio shown and is sourced from MSCI ESG Research, a leading provider of environmental, social and governance analysis and ratings.

| MSCI ESG RATING (AAA-CCC): | A |

| ESG-Qualityrating (0-10): | 6,736 |

| Environment Rating (0-10): | 5,286 |

| Social Rating (0-10): | 4,993 |

| Governance-Rating(0-10): | 6,355 |

| ESG rating in comparison group (0% lowest, 100% highest value): | 11,110 % |

| Peergroup: |

Equity Europe Sm&Mid Cap

(207 Fonds) |

| Coverage rate ESG rating: | 84,794 % |

| Weighted average CO₂ intensity (tons of CO₂ per 1 million US dollars in sales): | 49,177 |

Portfolio allocation according to ESG rating of individual securities

Report date: 30/04/2024

- The fiscal treatment depends on the personal circumstances of the respective client and can be subject of change in the future.

- is proprietary to Morningstar and/or ist content providers may not be copied or distributed and is not warranted ob e accurate, complete or timely. Neither Morningstar nor ist content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Perfomance Chart

Performance in Percent

Rolling performance in %

Risk metrics (16/05/2024) |

|

|---|---|

| Standard Deviation (2 years): | 17,06 % |

| Tracking Error (1 years): | - |

| Value at Risk (99% / 20 days): | -11,06 % |

| Maximum Drawdown (1 year): | -13,34 % |

| Sharpe Ratio (2 years): | -0,24 |

| Correlation (1 years): | - |

| Beta (1 years): | - |

| Treynor Ratio (1 years): | - |

Country allocation total portfolio (% NAV)

*Note: Cash position is included here because it is not assigned to any country or currency.

Data: Anevis Solutions GmbH, own illustration 30/04/2024

Top Country Allocation in % of Fund Volume (30/04/2024) |

|

|---|---|

| Germany | 66,89 % |

| Switzerland | 12,66 % |

| Austria | 4,92 % |

| Netherlands | 3,57 % |

| Sweden | 2,59 % |

Asset allocation in % of the fund volume (30/04/2024) |

|

|---|---|

| Stocks | 97,94 % |

| Cash | 2,06 % |

Investment strategy

The fund focuses on high-growth and innovative companies (“hidden champions”) in the DACH region (Germany, Austria, and Switzerland). In terms of market capitalisation, the fund mainly invests in small- and mid-cap companies. We have an active bottom-up approach that primarily focuses on fundamental analysis of the companies. The fund invests in equities with high, sustainable, and stable earnings growth. The aim is an attractive risk-reward profile with low maximum drawdown and low volatility.

Chances

- With over 1,500 companies, the German-speaking region is the core region of the "hidden champions" (unknown companies with a leading market position).

- The Mittelstand is the innovation, technology and economic engine of the D-A-CH region.

- Small and medium-sized companies usually have a higher growth potential than large corporations.

- The D-A-CH region is characterised by a stable domestic economy, high legal security and export strength, spread across many sectors.

Risks

- In addition to market price risks (equity, interest rate and currency risks), there are country and creditworthiness risks, e.g. a recession of the European economies.

- Small and medium-sized companies are traded less on the stock exchanges than large corporations. Their share prices can therefore fluctuate more than those of large companies.

- Share prices can fluctuate relatively strongly due to market, currency and individual value factors.

Target group

Der Fonds eignet sich für Anleger

- who prefer European titles

- who would like to invest in medium-sized companies

- with a medium-to-long term investment horizon

Der Fonds eignet sich nicht für Anleger

- who seek safe yields

- who will not accept any increased value

- with a short-term investment horizon

Monthly Commentary

The majority of European stock markets experienced a setback in April, although there were also positive exceptions, including the Swiss and Austrian markets. Contrary to expectations, the eurozone economy avoided a technical recession in the first quarter and grew by 0.3% compared to the previous year. However, the stock markets were burdened by the fact that hopes of an imminent reduction in key interest rates in the USA turned into expectations of having to live with the current interest rate plateau for even longer in view of the further rise in inflation. For the eurozone, however, the markets continue to expect a first rate cut in June, as inflation is still on the decline here - the inflation rate stagnated at 2.4% in April and core inflation fell from 2.9% to 2.7% (both compared to the same month last year). The greatest inflationary pressure in the eurozone recently came from the services sector, which grew by 3.7% year-on-year. The Purchasing Managers' Index for this sector has been in expansionary territory since February of this year, i.e. above the threshold of 50 points, and rose to 53.3 (from 52.9) points in April. In contrast, the Purchasing Managers' Index for the manufacturing sector has remained stable in recessionary territory since August 2022 and currently stands at 45.7 points, signalling a shrinking economy. What also kept the markets on tenterhooks was Iran's attack on Israel and the Israeli response, which caused the VIX volatility index to spike to its highest level of the year and briefly drove up the oil price. The DJE - Mittelstand & Innovation fell by -2.64% in this market environment. The automotive, technology and financial services sectors had a particularly negative impact on performance, partly due to poor corporate news and quarterly figures as well as reduced profit forecasts for automotive companies and partly due to the environment of rising interest rates, which weighed on the technology sector. On the other hand, the energy, basic materials and food & beverages sectors performed particularly well. Energy and basic materials benefited from the rise in commodity prices in the meantime. Industrial and precious metals also rose. The fund management adjusted the allocation over the course of the month and increased the weighting of the media, travel & leisure and chemicals sectors. In return, it reduced the Technology, Industrials, Healthcare and Drugstore & Food sectors. As a result, the fund's investment ratio fell from 100.20% to 97.94%.